Structuring Delivery Ownership Across Fintech Systems

- Jun 12

- 9 min read

Updated: 12 hours ago

Contents

Regulated Fintech Delivery Needs a Single Accountable Owner

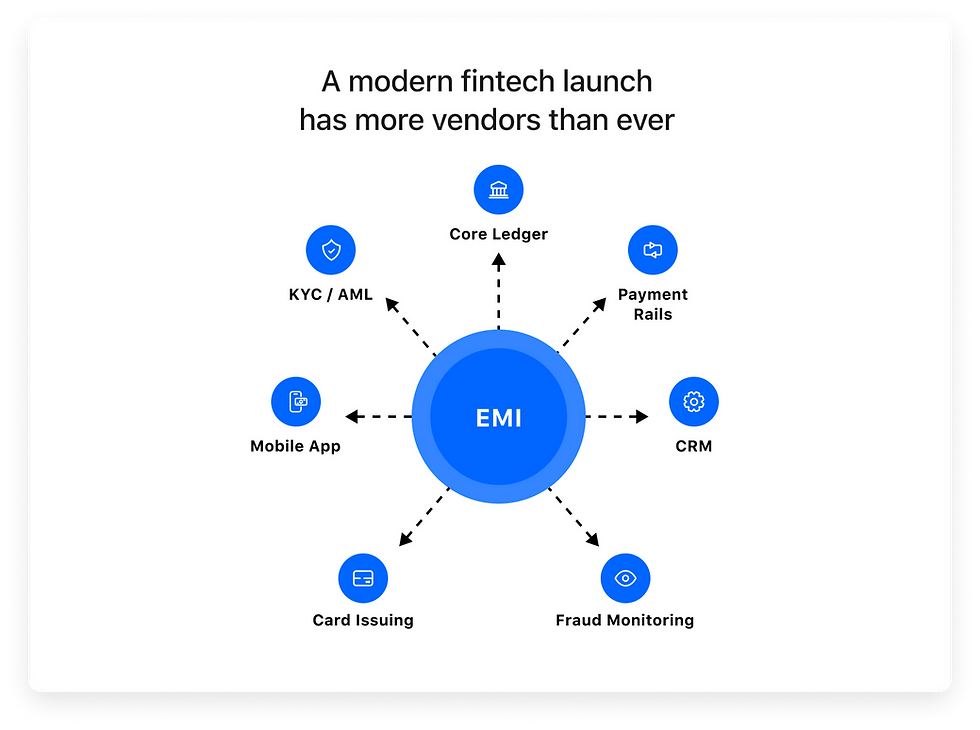

The modern fintech landscape is built on a paradox. On one hand, the industry has never had more access to specialized, high performance technology. On the other hand, the difficulty of actually launching a regulated service has increased. This difficulty does not stem from a lack of tools, but from a crisis of coordination. When an institution decides to build a new digital bank or payment service, it no longer looks for a single vendor to provide every piece of the puzzle. Instead, it assembles a stack. It selects a provider for the ledger, another for card issuing, a third for identity verification, and perhaps a fourth for international payment rails.

In a boardroom, this approach looks like the ultimate strategic advantage. It promises the ability to select the best possible partner for every niche. By breaking the project into smaller pieces, the institution can move faster and avoid the trap of being locked into a single monolithic provider. Product teams love this modularity because it allows them to design a unique proposition without being limited by the constraints of an old fashioned core banking system. Technology leaders appreciate the flexibility because it allows them to replace individual components as the market evolves.

However, as the program moves from the planning stage into the reality of implementation, the hidden costs of this fragmentation begin to surface. The primary challenge is that when you unbundle the technology, you also unbundle the accountability. In a traditional model, there was one throat to choke if the system failed. In a modular model, the responsibility for the final outcome often disappears into the gaps between the various providers. This is the challenge of delivery ownership. Without a clear center of gravity, a fragmented project will eventually succumb to its own complexity.

The Problem of Specialist Gravity

Every vendor in a project involving multiple providers operates within its own sphere of influence. We can think of this as specialist gravity. A specialist provider is hired because they are excellent at one specific thing. A card issuing partner is an expert in authorization logic and network connectivity. A KYC provider is an expert in identity document scanning and database matching. Their internal success metrics are tied strictly to their own domain.

The card issuer is successful if their APIs stay up and their plastic cards are delivered on time. They are fundamentally indifferent to how their data impacts the internal general ledger of the bank at three in the morning during a weekend reconciliation run. Similarly, the KYC provider is successful if their identity checks are accurate. They are not concerned with how a pending status in their system creates a customer support nightmare in the mobile app because the two systems do not communicate the specific reason for a delay.

This is the natural state of a specialist. They optimize for their own contract and their own narrow scope. When you have five or six such specialists working on a single launch, you do not have a cohesive team. You have five or six separate orbits. The institution usually assumes that these orbits will naturally converge into a launchable product, but they rarely do. Left to their own devices, these separate workstreams will drift apart.

The spaces between the vendors become a no mans land where the most dangerous risks live. Who owns the integrity of the data between the ledger and the card processor? Who owns the experience of the customer when a transaction is flagged for fraud but the notification engine belongs to a third party? In a fragmented delivery model, the institution often finds itself acting as a full time shock absorber. It spends the majority of its time reconciling the different interpretations and priorities of its various suppliers rather than focusing on the product itself.

The Asymmetry of Readiness

One of the most common ways a fragmented project fails is through a phenomenon we can call the asymmetry of readiness. In any complex fintech project, not all workstreams mature at the same pace. In a regulated environment, a program is only as ready as its slowest and least visible component.

During the early stages of a project, progress feels rapid. The product team is creating beautiful user interfaces. The developers are making successful API calls to the sandbox environments provided by the vendors. On a status report, every line item looks green. This is because the visible parts of a fintech product are often the easiest to build. Designing a screen or connecting to an API is a well understood task.

The invisible parts of the service take much longer. These are the operational and regulatory guts of the business. They include exception handling, dispute management, regulatory reporting, and settlement reconciliation. These areas are difficult because they require a deep understanding of how the institution will actually absorb the technology once it is live.

A customer journey might look perfect in a demo but fail in production if the back office team lacks the tools to handle a complex dispute or evidence a control decision to an auditor. The danger is that the project builds up a massive amount of readiness debt. The technical integrations move forward, but the operational environment around them remains immature. You end up with a product that looks ready for launch during a presentation but would crumble under the weight of real customers and the support tickets they generate.

Programs that lack a central delivery owner usually do not discover this asymmetry until they reach the final stages of testing. By then, the launch date is often fixed and the marketing budget has been spent. The institution is forced to launch with a culture of manual workarounds that becomes impossible to scale.

The High Cost of the Ownership Gap

When ownership is fragmented, the cost of the project does not just increase linearly, it explodes. This is not because the vendors are charging more than they agreed, but because the cost of uncertainty becomes the dominant expense. Most delivery problems arrive quietly. They start as a small assumption made by an engineer at one provider about how another provider handles a specific data field. Because there is no central authority to validate that assumption, it remains unchallenged for months.

As the project nears completion, these assumptions start colliding. This leads to a period we can call the reconcile phase. This is the point where the institution realizes that two different providers have completely different interpretations of the same requirement. At this stage, the institution has two choices. It can delay the launch to rewrite the integration, which is expensive and embarrassing, or it can hire more people to manually bridge the gap between the systems, which is even more expensive in the long run.

This is why thin project management is insufficient for regulated fintech. You do not need someone to merely tell you that a task is late. You need someone who can tell you that the task itself is defined incorrectly and will fail when it hits the compliance environment. You need implementation ownership that understands the logic of the business and the requirements of the regulator, not just the timing of the tasks on a spreadsheet.

Establishing a Center of Gravity

To survive a project involving multiple vendors, a program needs a center of gravity. This is a single team or partner that owns the final outcome regardless of which vendor provides which component. Ownership in this context is not about control in a negative sense. It is about accountability for the integration of responsibility. This center of gravity performs several critical functions that standard project managers often miss.

First, it curates the sequence of risk. In a standard project, teams often do the easy things first to show progress. In a high stakes fintech launch, a delivery owner forces the hardest and most complex questions to the front of the queue. They solve the settlement logic before they polish the login screen. They finalize the anti money laundering workflow before they worry about the rewards program. They de risk the program by tackling the regulatory and operational hurdles while there is still time to adjust the architecture.

Second, it sets standards for testing that are ready for production. Most vendors test to satisfy their own contract. They want to show that their API works as documented. A delivery owner tests to satisfy the live service. This means testing the messy middle. They look at what happens during high latency, partial failures, data corruption, and human error. They create a testing environment that reflects the actual operating reality of the bank, not the idealized world of a vendors sandbox.

Third, it owns the no mans land between providers. The delivery owner is the one who defines the handshake between systems. They do not wait for different vendors to talk to each other. They dictate the protocol for that conversation. They ensure that if a transaction fails in the ledger, the notification engine knows exactly what to tell the customer and the support dashboard shows exactly what the agent needs to see to resolve the issue.

Governance Beyond the Calendar

In many organizations, governance is treated as a series of meetings. This is a mistake. Governance should be a mechanism for closure. In most fintech projects, governance is performative. People meet once a week to look at a deck where most of the slides are green. This creates a false sense of security.

Useful governance in a regulated environment requires explicit command. Risks should not just be noted in a log. They should be moved to a decision maker who has the authority to change the scope or the budget to fix the root cause. Furthermore, the people who will actually run the service after it launches must have the power to sign off on readiness. If the support leads, the risk officers, and the finance managers are not confident, the project is not finished.

Readiness should be judged by evidence rather than opinion. A statement that an integration is ninety percent done is an opinion. A statement that the team has successfully reconciled one thousand test transactions across all three systems with zero manual intervention is evidence. Strong governance does not add weight or bureaucracy to a program. In fact, it makes the program faster because it removes the uncertainty that causes teams to hesitate.

Raising the Bar for Delivery Partners

The era of the body shop vendor is ending. In the past, a bank might hire a partner to provide ten developers or five testers. This model works for simple software, but it fails in regulated fintech because it leaves the burden of delivery ownership entirely on the shoulders of the bank. A modern delivery partner must contribute more than just effort. They must contribute judgment.

Real value in a fintech partner is found in their experience with failure. You want a partner who has seen a settlement engine fail at scale and who knows why a specific provider might struggle in a particular jurisdiction. You want someone who understands how to build an integration layer that will not break the first time the network has a brief lag.

This partner needs to stay close to the product even after the launch. In fintech, the launch is just the beginning of the learning process. The moment real customers start using the service, the organization will find rough edges that no amount of testing could have predicted. Customer behavior reveals unexpected patterns. Operational load exposes weak spots. If the delivery knowledge evaporates the day after launch, the institution is left in a vulnerable position. A true partner remains involved to turn that live feedback into controlled and iterative improvements.

The Strategy for Execution

This is the specific execution problem that Velmie addresses. We recognize that the software problem in fintech is largely solved. There is no shortage of ledgers or payment rails in the market. The execution problem, however, is more acute than ever. Velmie does not just offer a suite of banking modules. We offer an implementation logic.

Our value to a regulated institution is not just in the code we write, but in the way we organize the design, the integration, the testing, and the release. We act as that center of gravity. Because we have scope across the entire stack, from the customer facing apps to the deep end infrastructure for payments and compliance, we can see the ownership gaps before they become expensive failures.

For an institution, working with a partner in this way means you are not just buying a set of components. You are buying a path to a stable and operable service. We take responsibility for the coordination of the various moving parts, ensuring that when you launch, you are in control of the outcome.

Conclusion

Regulated fintech is difficult because it requires the perfect alignment of technology, regulation, and operations. In an era where the technology stack is increasingly fragmented, that alignment does not happen by accident. Delivery ownership is the difference between a program that looks good on paper and a service that works in production. It is the difference between a launch that is a celebration and a launch that is a crisis.

The institutions that will win in the coming years are not necessarily the ones with the most innovative technology. They are the ones that have the discipline to establish a clear center of delivery ownership. By ensuring that the complexity of the tech never compromises the stability of the service, they create a foundation for lasting growth. Fragmentation is a reality of the modern market, but ownership is the only way to manage it effectively. The goal is to move from a collection of parts to a coherent service that can be run, extended, and trusted by the market.