From Pixels to Plumbing: Aligning Front-End with Backend Reality

- 6 days ago

- 5 min read

Contents

The visual appeal of a mobile banking app is often a distraction from the structural integrity of the service itself. In high stakes financial environments, a polished interface acts as a mask for an immature backend. While a prototype can simulate a smooth transaction in a boardroom, the reality of a regulated product is found in the response times of the issuer, the clearing states of a payment, and the rigid logic of compliance checks. When front-end work outpaces the development of these core systems, the program accumulates a dangerous gap between customer expectation and technical execution.

This gap is rarely visible during a demo where data is idealized. The problems surface only when the institution attempts to turn attractive journeys into production flows. At that point, clean design assumptions collide with the technical friction of live banking infrastructure. A roadmap that prioritizes visual milestones over operating logic eventually reaches a point of zero delivery certainty.

The Architecture of Reliability

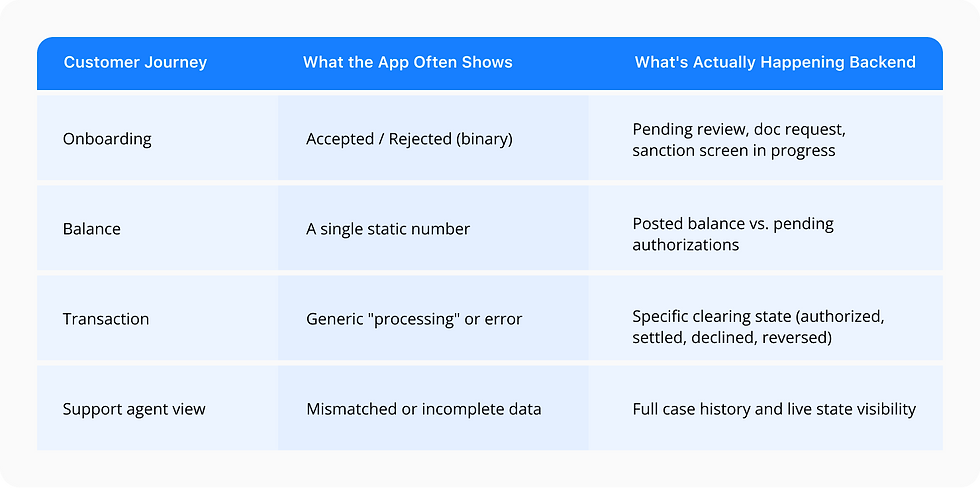

Reliability does not begin with the interface. It begins with the state machine that governs every customer interaction. In a design file, onboarding is often treated as a binary outcome where a user is either accepted or rejected. In a live environment, this is rarely true. An application might move into a pending review state, require additional documentation, or pass an identity check but fail a sanction screen.

If the channel team has not built the app to reflect these granular states, the customer experience collapses. When a journey enters a state the app does not recognize, the interface usually defaults to a generic error message. This is a communication failure. The backend knows exactly what is occurring, but the app is not designed to tell the truth about the service model.

The same logic applies to wallet data. A balance shown on a screen is a claim, not a statistical fact. Its value depends on posting logic and settlement timing. If the app fails to account for pending authorizations, the customer will eventually attempt a transaction that is declined. Transaction handling is equally unforgiving. A customer cares less about the aesthetics of a payment button than they do about the clarity of their money status when a payment is delayed or reversed.

The Reality of System Drift

Customers recognize when a product is out of alignment through the practical failures of the service. Onboarding flows that stall without context, payments that enter inexplicable states, and discrepancies between app balances and support agent data all expose backend uncertainty.

These disconnects are symptoms of a delivery model that treated the app as an entity separate from the service logic. For a regulated institution, these issues scale quickly. A technical glitch in a banking app is a control issue. If thousands of users encounter a stuck transaction state because of a backend misalignment, the support center is overwhelmed within an hour. This operational weakness eventually draws regulatory attention. App quality, support stability, and compliance confidence are all anchored to the same underlying technical maturity.

Redefining Ownership in the Stack

Achieving a production grade channel requires a unified delivery model where the app, the APIs, and the service logic function as a single unit. The industry must move away from the idea that front end and backend roadmaps can exist in isolation.

Product planning should be driven by backend readiness. If the issuing integration cannot support a specific card control, that feature has no place in the app design. Release planning must be synchronized to ensure that mobile updates do not assume backend logic that has yet to clear production governance. Strong ownership closes this distance early in the lifecycle so that the customer is not the first person to discover a gap in the service model.

Back Office Tools as Front-End Features

Neglecting the back office is a significant mistake in fintech delivery. The support team is the human interface of the service, and when the technology is opaque, they inherit the burden of explaining it. To function effectively, agents need a servicing layer that provides deep state visibility and clear case history.

If an agent sees a different data set than the customer, or cannot identify why a journey stopped, they cannot resolve the issue. They are forced to admit ignorance, which is the fastest way to destroy trust in a financial brand. Back office design is an essential part of channel design. An elegant customer journey still creates massive operational costs if the internal side is neglected. Good mobile delivery treats back office clarity as a primary product requirement.

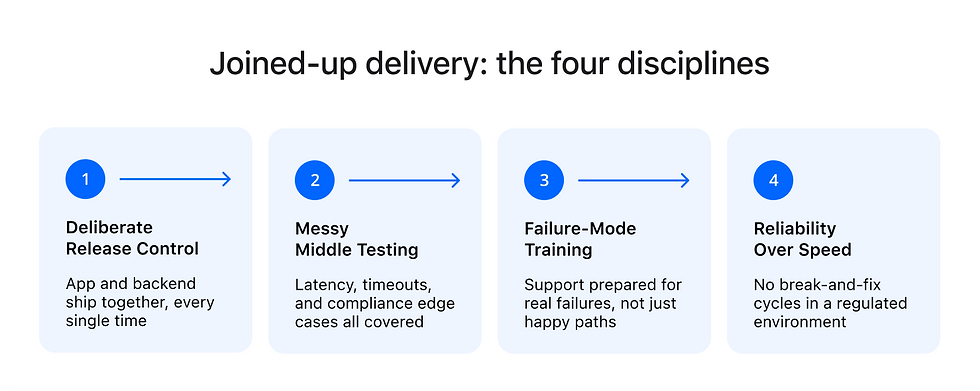

Principles of Joined-Up Delivery

A mature delivery model follows a single plan across every layer. It avoids asking the mobile app to carry assumptions the backend cannot support and rejects the idea of release management as a handoff between disconnected teams.

This requires specific disciplines:

• Release control must stay deliberate:

The app and backend move in lockstep.

• Core flows must be tested for the messy middle:

Testing must include high latency, partial timeouts, and compliance edge cases.

• Support teams must be trained on failure modes:

Preparation should focus on real world cases rather than idealized happy paths.

• Reliability must outweigh speed: A regulated service cannot afford a break and fix culture.

This is the standard for production grade mobile delivery. Design is important, but it is secondary to the integrity of the service.

Velmie Approach to Channel Integrity

Velmie views app reliability as a backend problem. We do not build screens in isolation and, instead, act as a systems integration partner that builds channels around the actual service model of the institution.

Our approach aligns front end delivery with backend reality from the start. Every state shown in a Velmie app is backed by a corresponding state in the core logic. By taking this end to end view, we reduce the gaps between user perception and system capability. This results in fewer surprises in production and a mobile experience that stays dependable as the product evolves. We work with regulated institutions to ensure their digital channels are true representations of a mature service.

Conclusion

The allure of a polished app is a trap. It is easy to confuse visual progress with technical readiness, but the consequences in regulated finance are severe. A mobile app is the window through which a customer views a complex machine. If the machine is broken, the window only serves to highlight the failure.

Success requires resisting the urge to lead with the app alone. Institutions must lead with a service model that is robust and fully integrated. Trust is built in the consistency of the experience. The organizations that survive the transition from a demo to a business are those that understand that the most important thing on a screen is the truth of the service behind it.